All individuals are eligible regardless of pre-existing conditions, prior usage, or age.

There are no deductibles or co-insurance amounts - 100% coverage.

There are no limits for the number of visits and treatments per practitioner.

You determine how much or how little you will spend in any given year. Budget control and no creeping premiums!

A Cost Plus Plan qualifies as a PHSP, and any premiums paid to a PHSP by a company are considered business expenses and 100% deductible against business income.

All premiums paid and benefits received are 100% tax free to the recipient whether it is the owner of the company or its employees.

A formal Private Health Services Plan (PHSP) agreement must be in place with a Third-Party Administrator (TPA) or Insurance Company.

Cost Plus Plans must be 100% funded through your company.

A Cost Plus Plan cannot be used to purchase additional insurance such as life insurance, Long-Term Disability or Critical Illness Insurance.

Benefits must meet income tax definitions of eligible expenses.

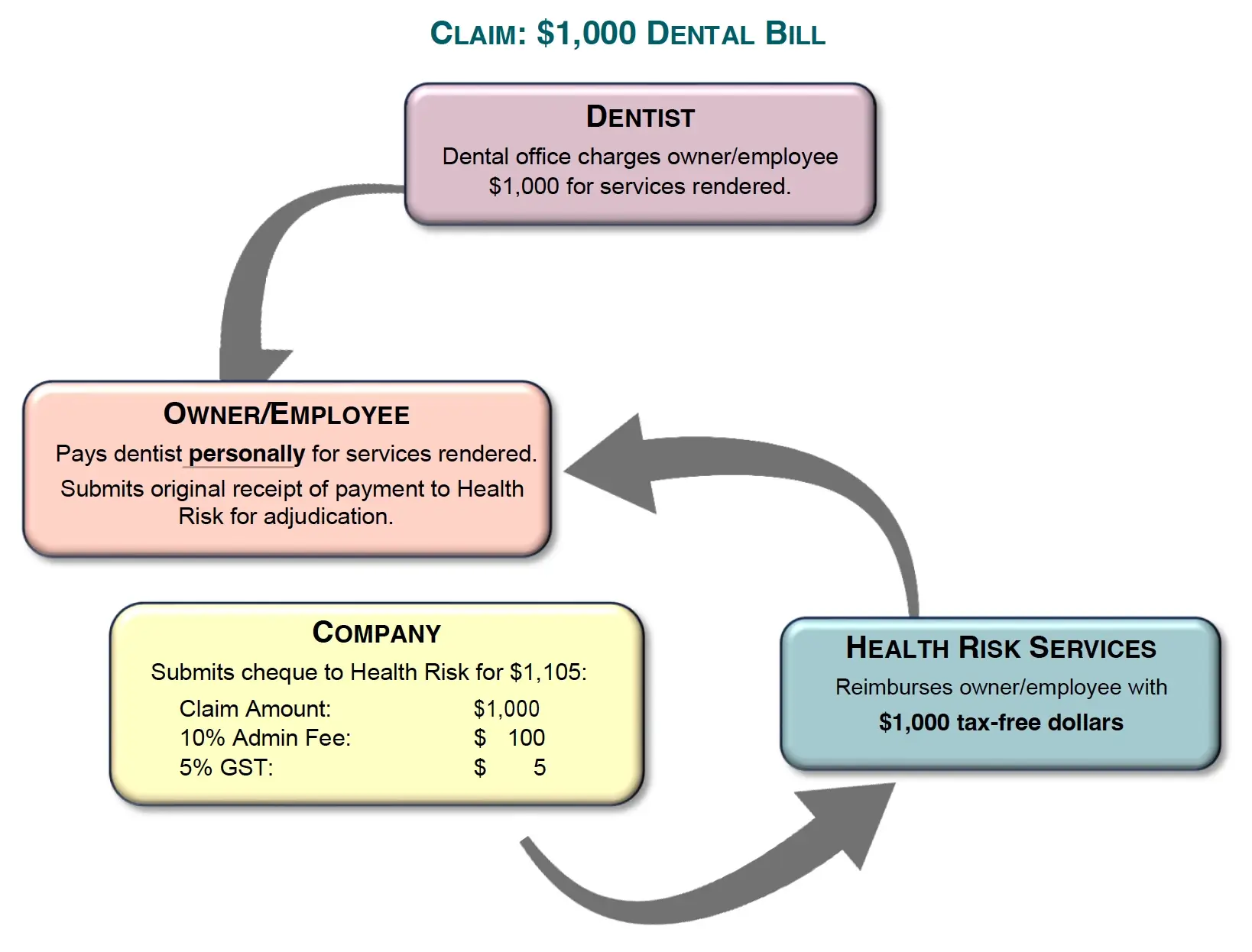

Pay-As-You-Go:

You submit your Cost Plus Claim Form along with your expense receipts to Health Risk Services. Your claim is adjudicated by our claim specialists to determine eligiblity and reimbursement. Your company will then receive an Invoice for the amount of the reimbursement due, plus the administration fee and GST. Once your company has paid the Invoice, Health Risk will reimburse you personally with your tax-free benefit amount.

Pre-Funded Plan:

Your company is Invoiced for the determined amount that you wish to use for “funding” your Cost Plus Plan. These funds are deposited into your plan Cost Plus Operating Account. The funds are then used to reimburse your claims as they are submitted avoiding any delays in processing. When your Operating Account is depleted, your company will once again be invoiced for additiona funding.

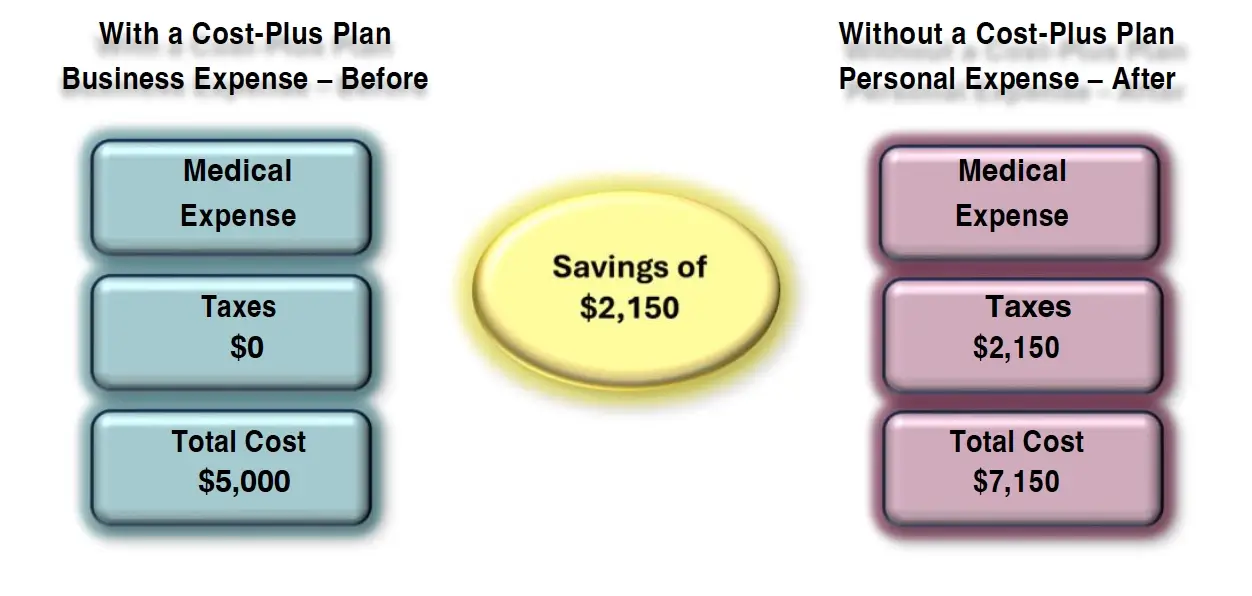

There is no formal plan in place, so you pay for all your medical expenses personally out of your pocket with tax dollars.

You implement a Cost Plus Plan in your business, which allows for 100% of all eligible medical expenses to be paid through your company.

We CARE about insisting that your plan stays current with CRA guidelines

We CARE about providing you with all the proper plan implementation documents for your corporation to ensure compliance with CRA.

We CARE about ensuring quick turnaround times for your claims.

We CARE about providing you with the convenience of direct deposit for your reimbursements.

We CARE about ensuring you are kept up to date on any legislation changes that may affect your Cost Plus Plan.